Would you like to save this?

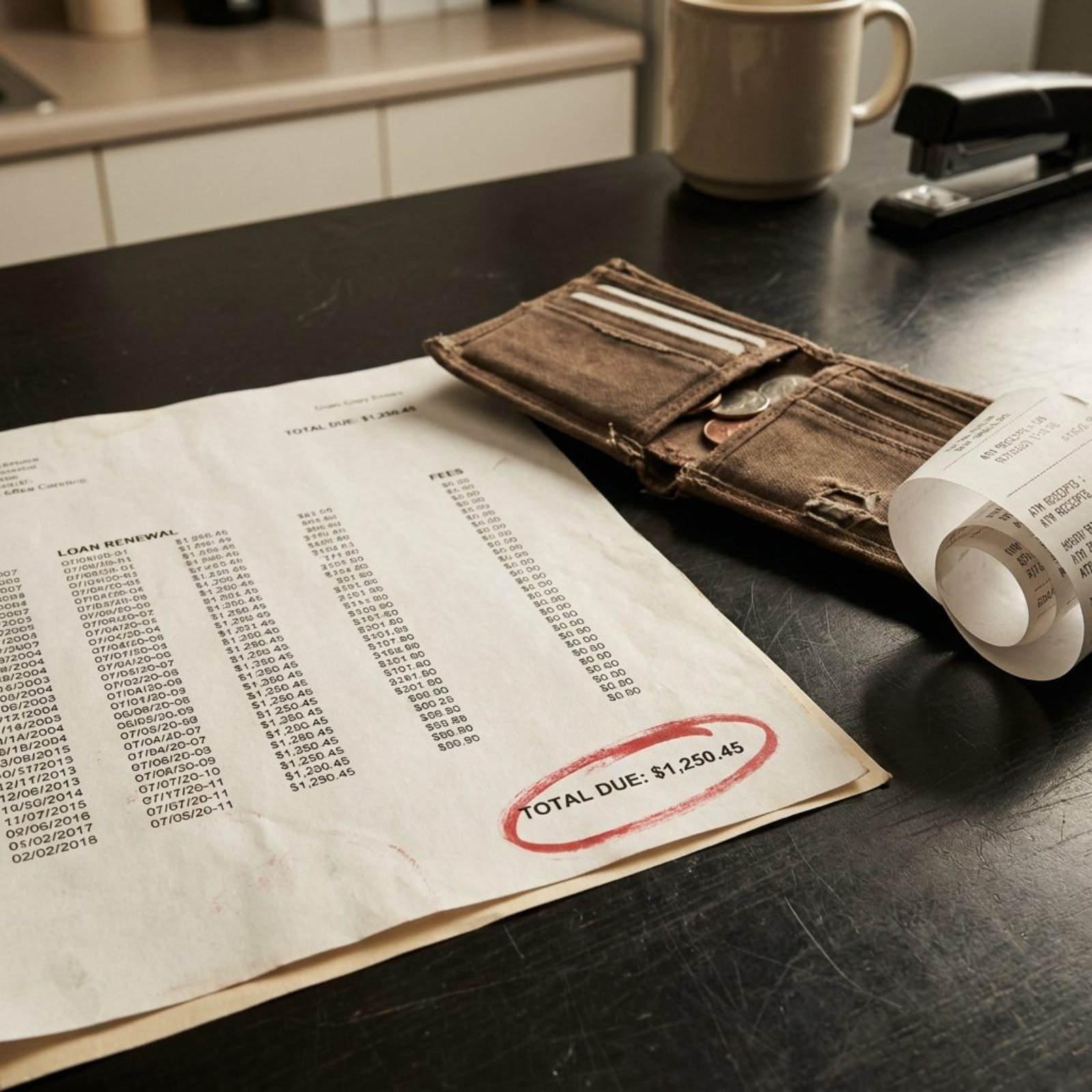

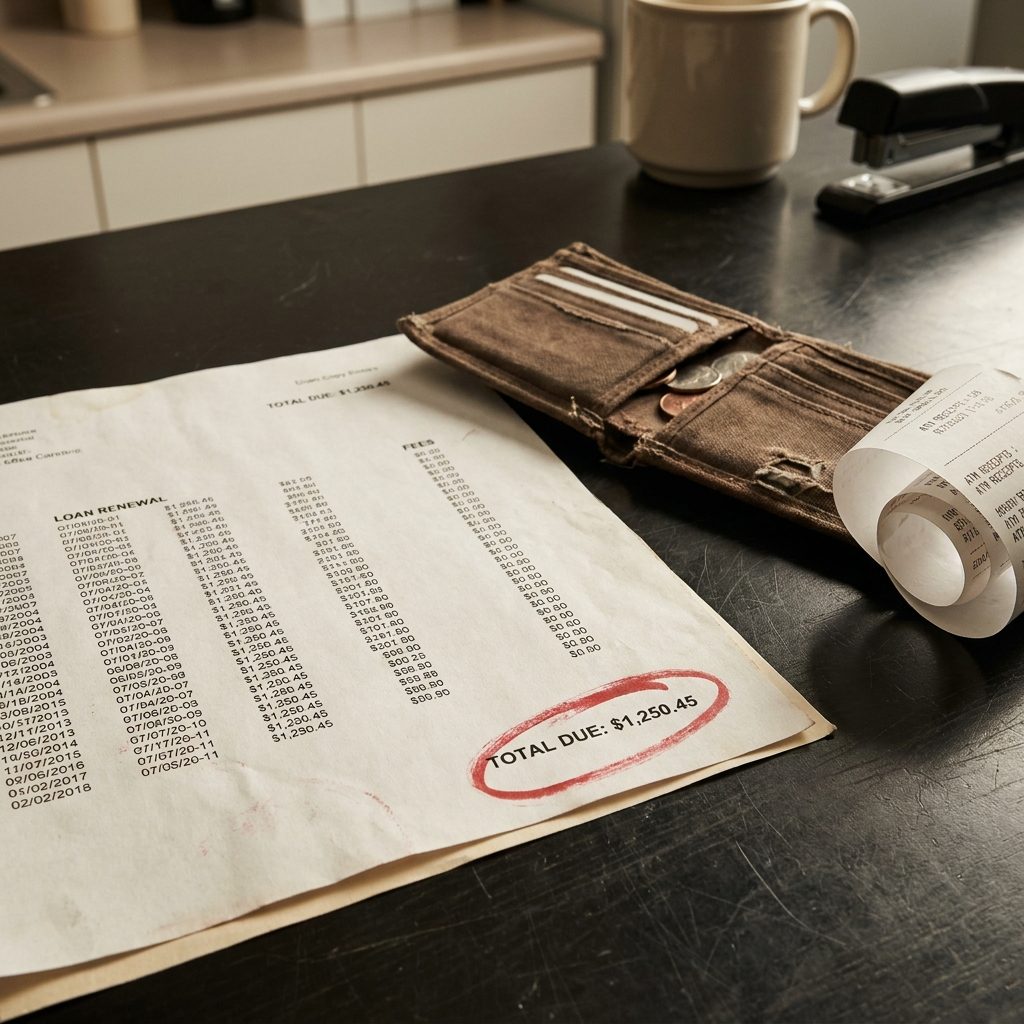

The bills don’t stop when the relationship does. They keep arriving, addressed to you, for things you never bought, accounts you never opened, loans you never signed for. Financial abuse can follow a survivor into a credit report, a mailbox, a rental application, or the first ordinary piece of life she tries to rebuild.

These are the debts survivors find weeks, months, sometimes years after getting out: the kind that make escape feel unfinished, as if the person she left still has one hand on the paperwork.

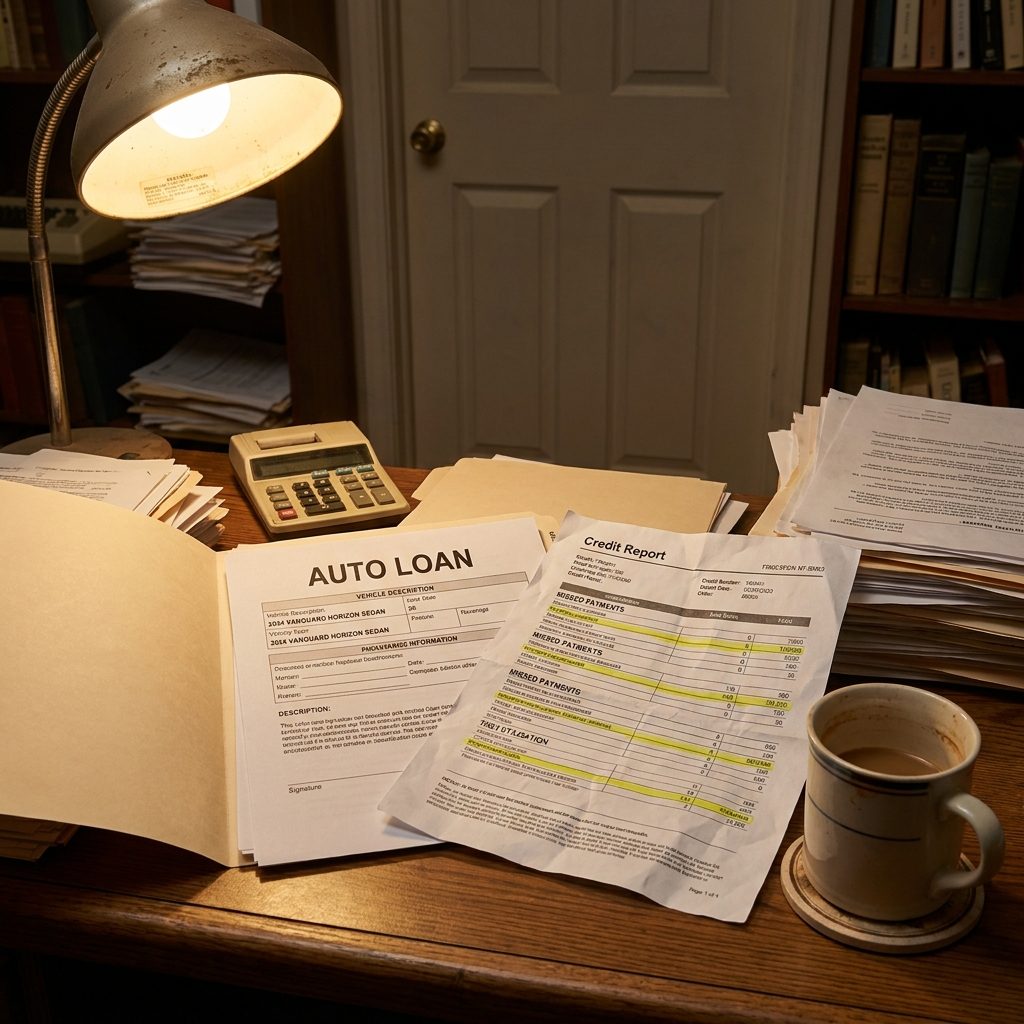

The Car Loan on a Vehicle You’ve Never Seen

It shows up on a credit report as a single line: a used car, financed five years ago, still carrying a balance. The vehicle was never yours. You never drove it, never signed for it, at least not knowingly. But your name is on the title, and the lender doesn’t care about the backstory.

Auto loans are one of the most common debts survivors find months after leaving, partly because they’re easy to open with a co-signer who doesn’t fully understand what they’re agreeing to, and partly because the abuser often kept driving the car long after the relationship ended, running up missed payments the whole time.

Credit Cards Opened in the Chaos of ‘Helping with Finances’

The pitch was always reasonable. Let me handle the bills. You’re bad with money. I just need your Social Security number to add you to the account. Except what got opened wasn’t a joint account, it was a new line of credit, in your name only, with a limit that got maxed inside six months.

Survivors often find three, four, sometimes six of these. Each one opened during a different “helpful” moment. Each one overdue by the time it surfaces.

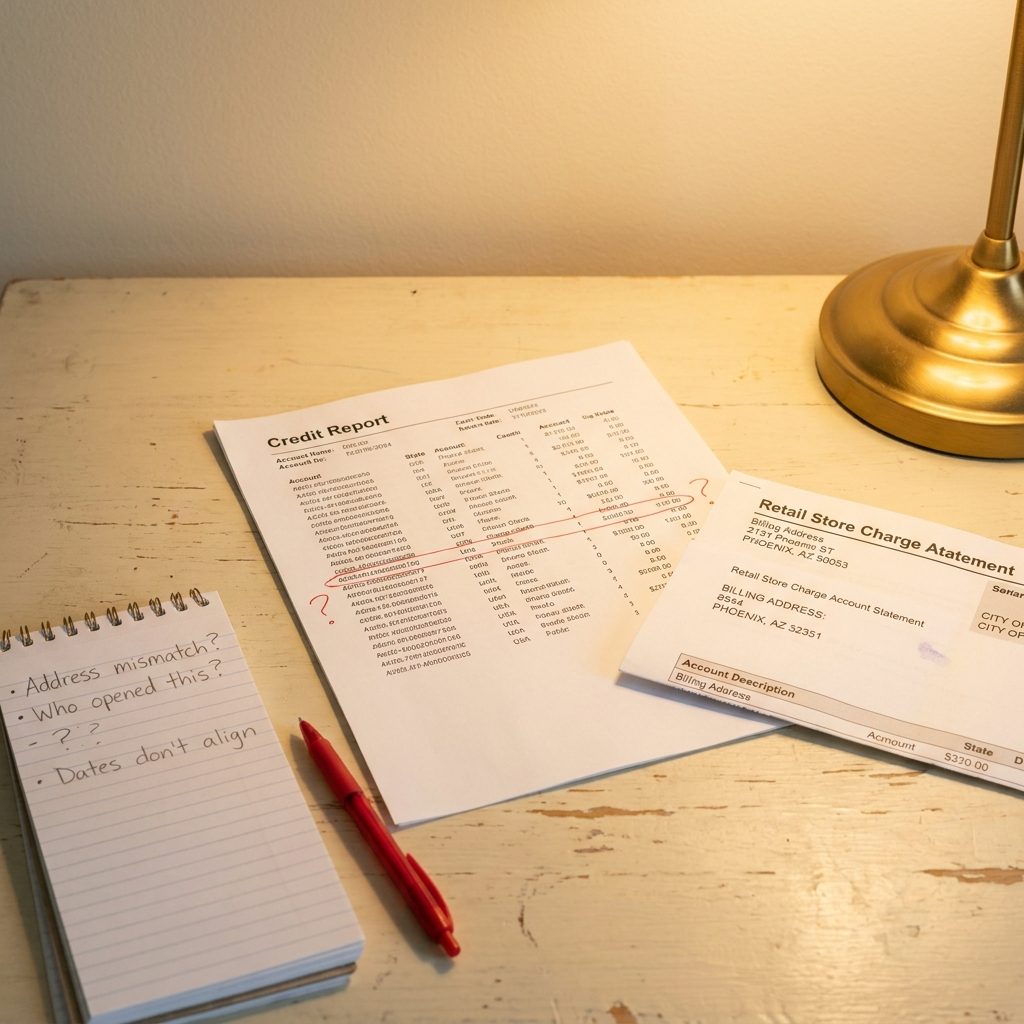

The Store Account at a Retailer in a City You’ve Never Visited

Retail store cards are easy to open and easy to miss. The credit limit is small enough that it flies under the radar on a report, $300, maybe $500, but the delinquency it carries punches well above its weight on a credit score.

When survivors find one at a store in a city they’ve never been to, it tends to reframe a lot of other memories. That trip the abuser took “for work.” The packages that showed up addressed to someone else.

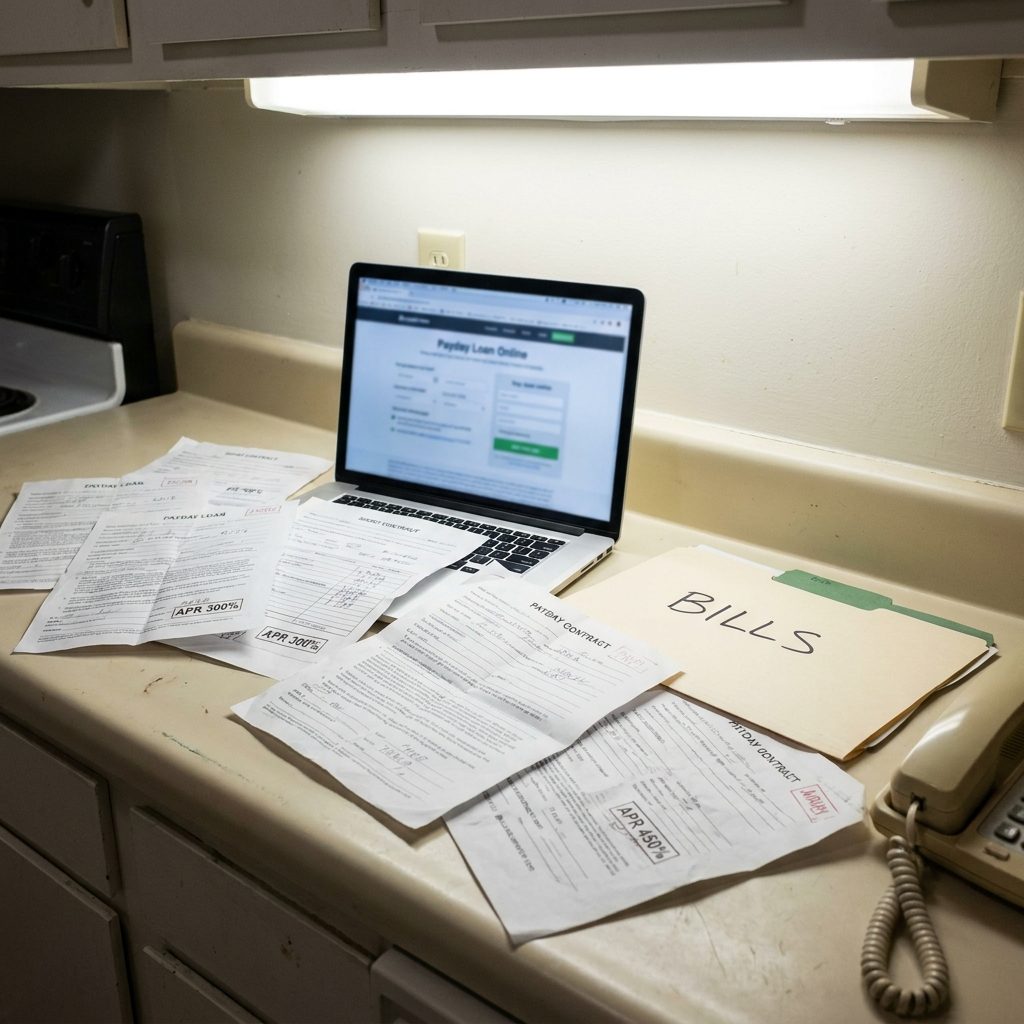

Payday Loans Taken Out During ‘Emergencies’ That Were Never Emergencies

Payday loan companies don’t ask many questions. They also don’t report to credit bureaus when accounts are current, which means survivors sometimes don’t find these until a collection agency picks up the debt and it lands on their report like a small bomb.

The amounts feel almost insulting given what they cost: $200, $350. But the fees stacked on top of fees, then handed off to collections, can swell them to amounts that take years to resolve. And the story attached to each one, the “emergency” that required it, rarely holds up to scrutiny.

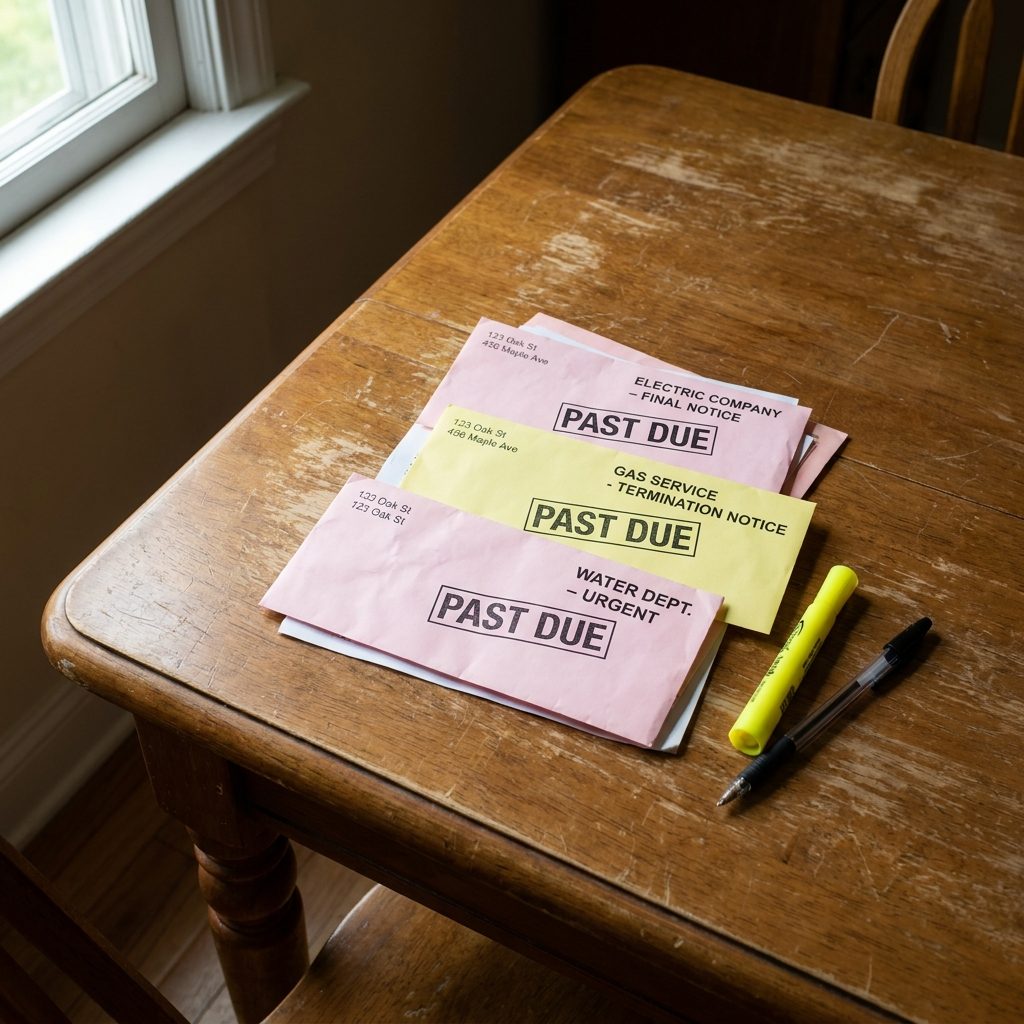

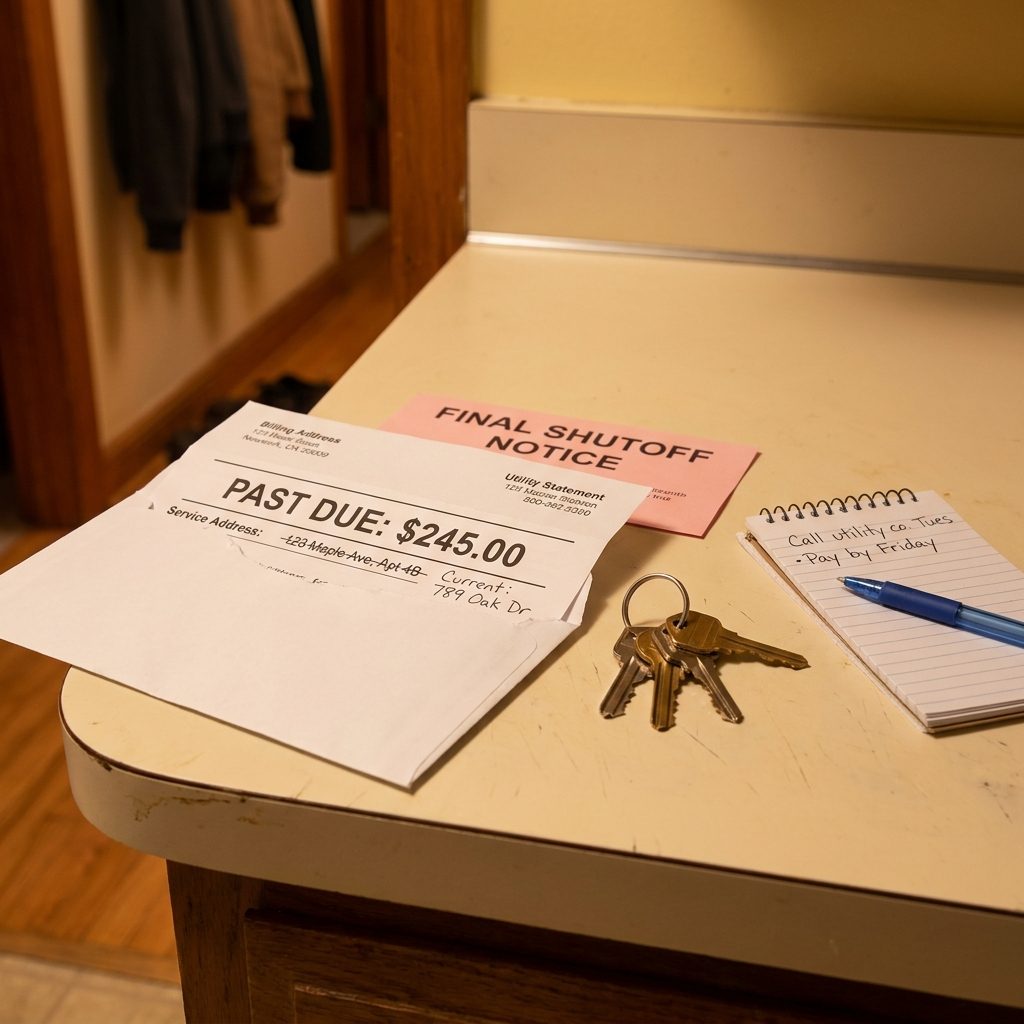

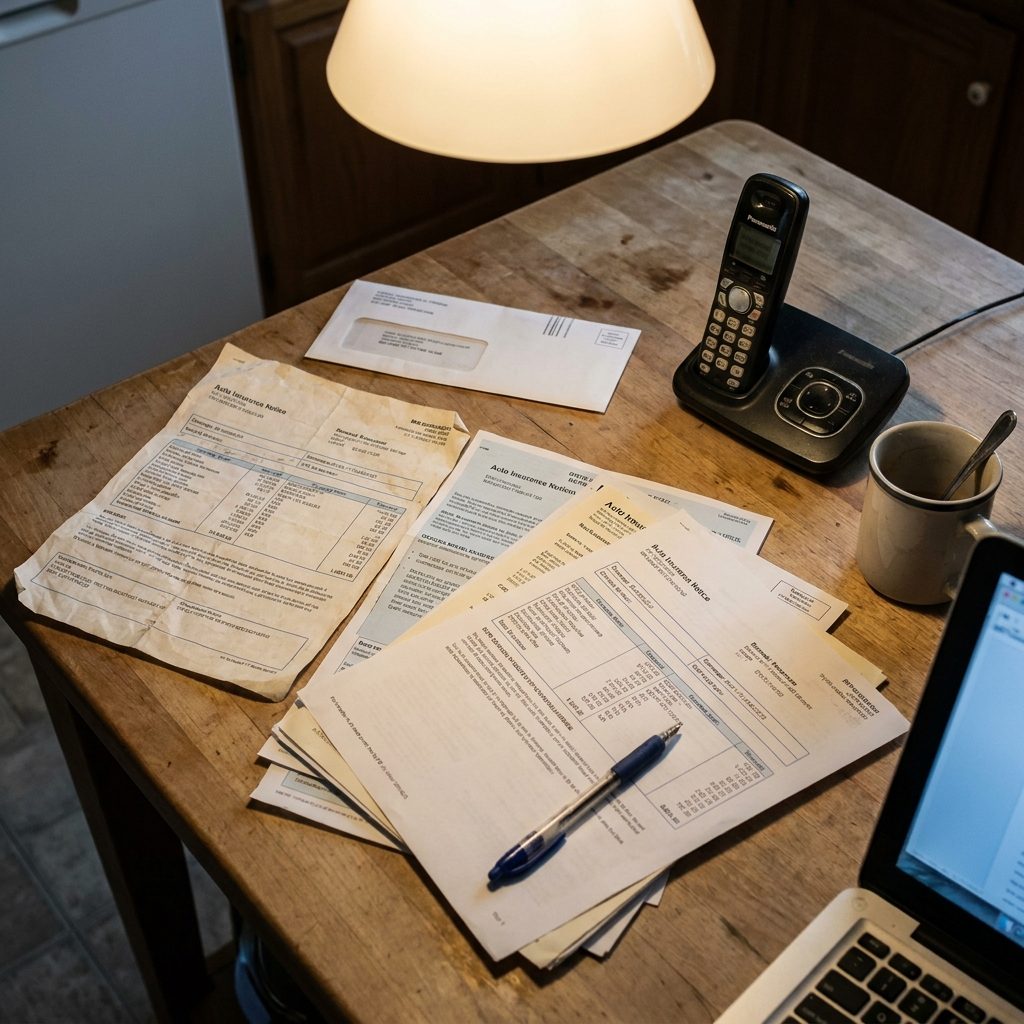

Utility Accounts Left Open and Unpaid at an Address You Moved Away From

When you leave a shared home, the utility accounts don’t automatically follow. If the abuser stayed or simply stopped paying, those final balances, electric, gas, water, sometimes internet, go to collections under whatever name was on the account. Which is often yours, because you were the one with the better credit when the service was first set up.

These debts are small enough to feel solvable. What they actually do is get reported to specialized screening databases that landlords use. Survivors discover this when they try to rent a new apartment and get flagged before the landlord even pulls a credit report.

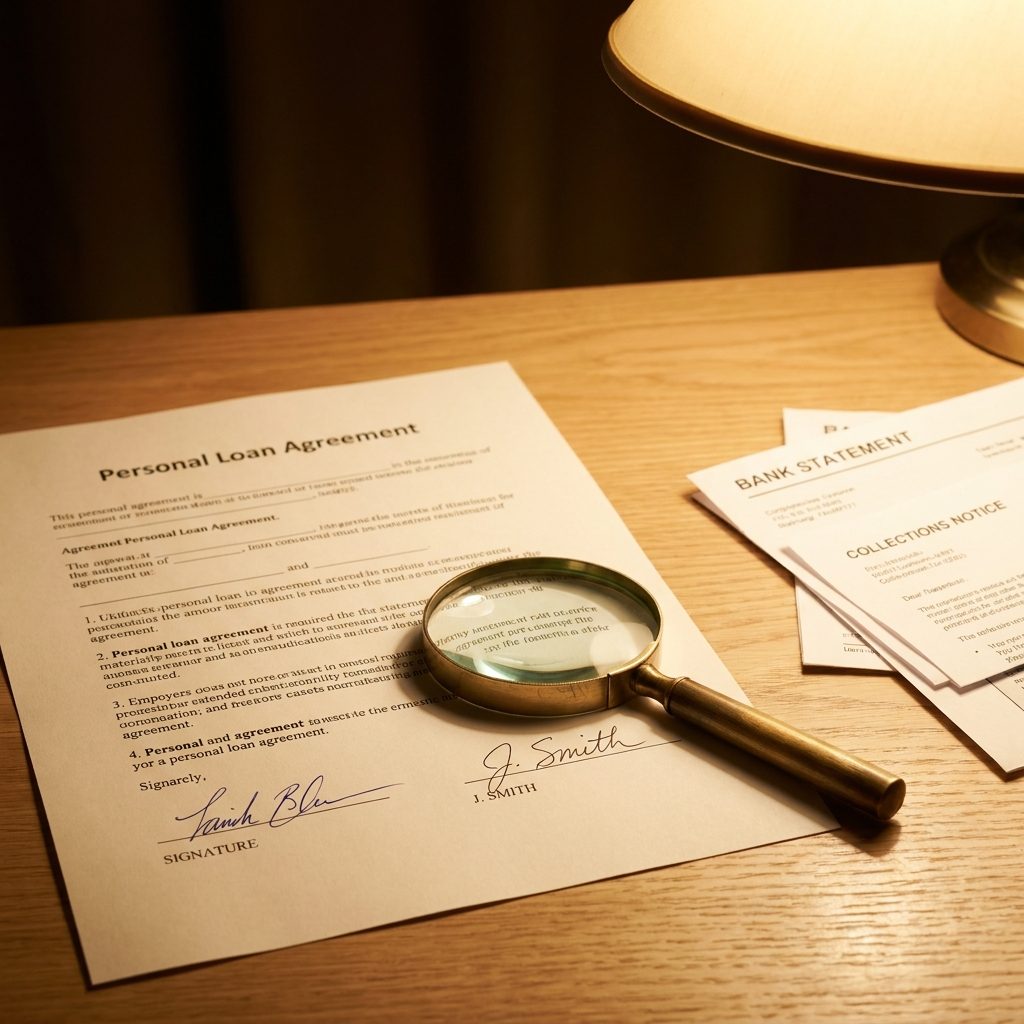

A Personal Loan Co-Signed ‘Just to Help a Friend of the Family’

It was presented as a favor. Sign here, it’s nothing, they’ll pay it back, it won’t affect you. And then it does, because when the “friend of the family” defaults, the lender comes for the co-signer. That’s the whole legal structure of co-signing, and the abuser understood that perfectly well.

Co-signed personal loans are harder to dispute because the signature is often genuinely the survivor’s. The question of whether that signature was coerced, forged, or obtained under false pretenses is a legal fight, not a phone call.

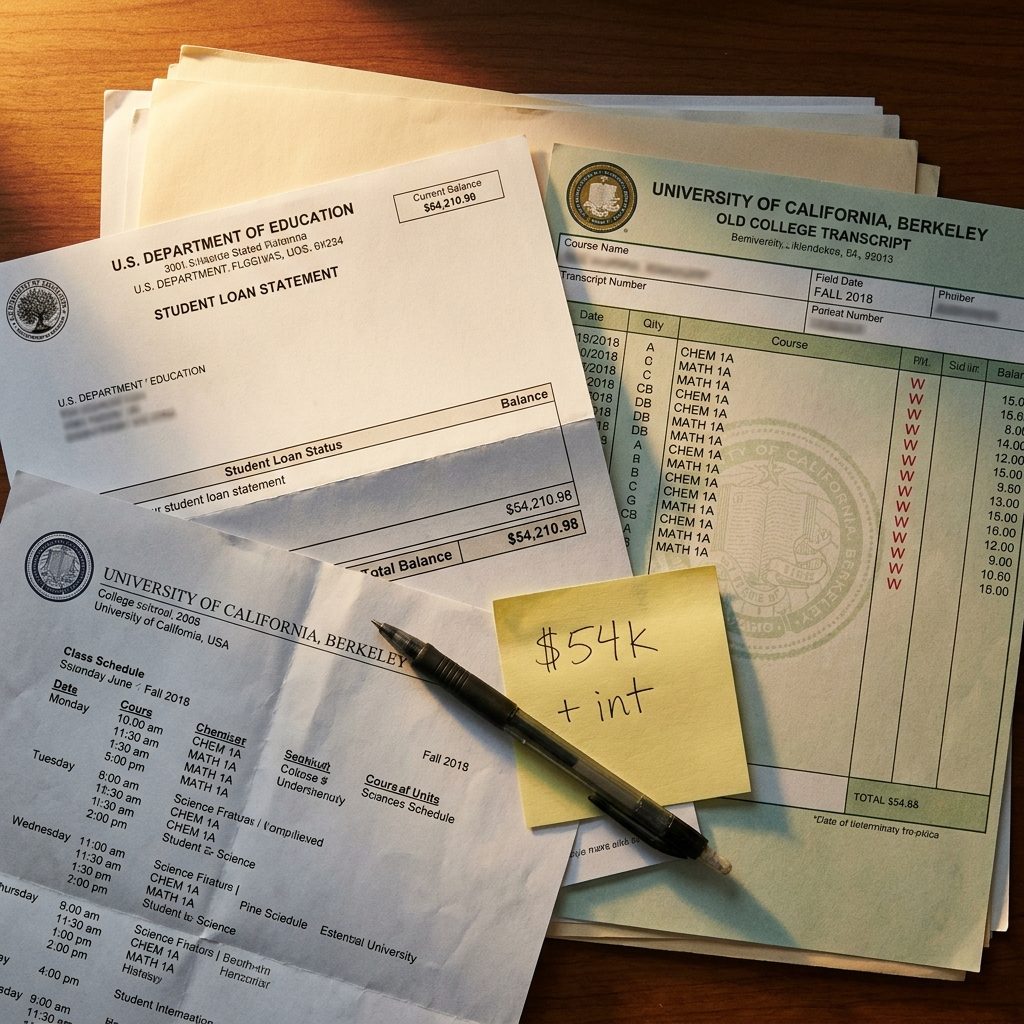

Student Loans for Enrollment at a School You Were Pressured to Quit

One semester. Sometimes two. The survivor enrolled, took out federal loans, and then the abuser made finishing impossible, through sabotage, relocation, manufactured crises, or plain prohibition. Withdrawal means the aid doesn’t get returned proportionally. The loans stay. The credits don’t count toward a degree.

Years later, those loan balances surface in collections or in repayment notices from a servicer the survivor never dealt with directly. The education never happened. The debt is very real.

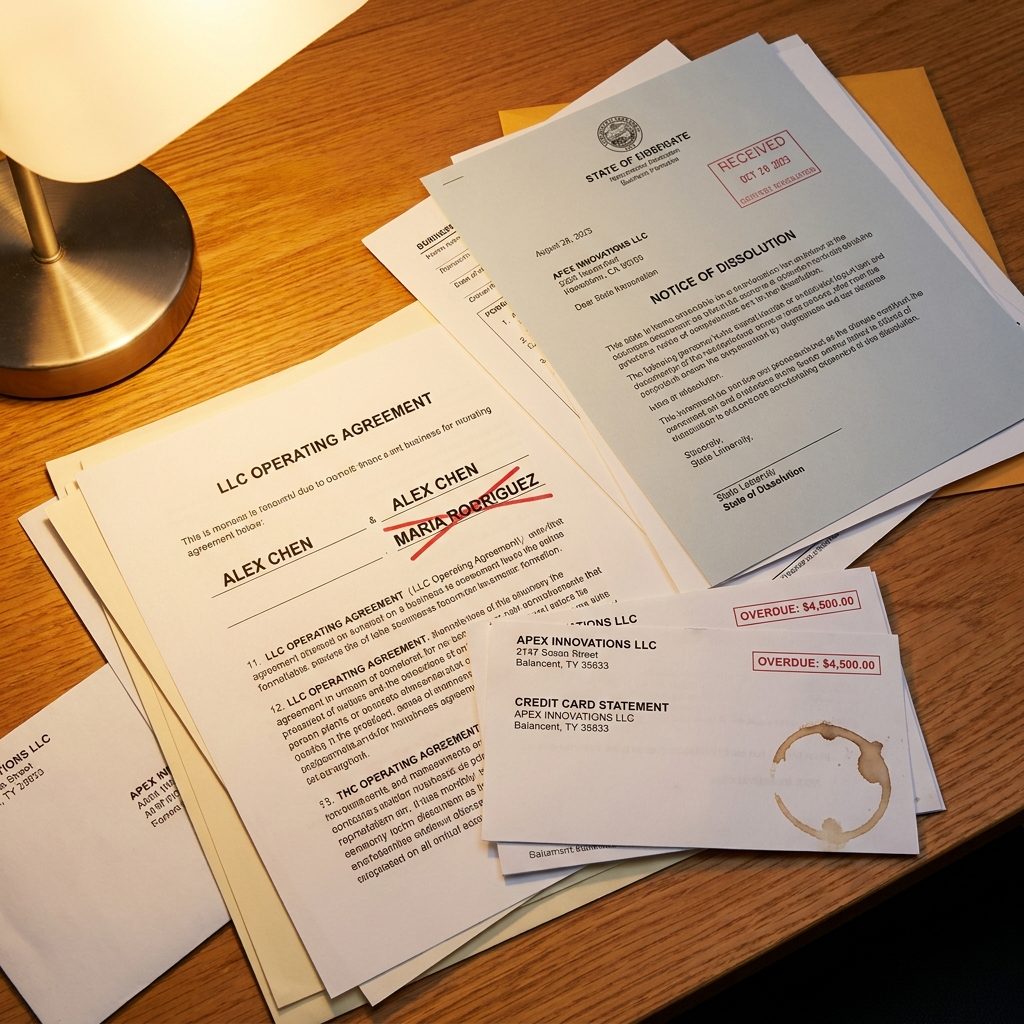

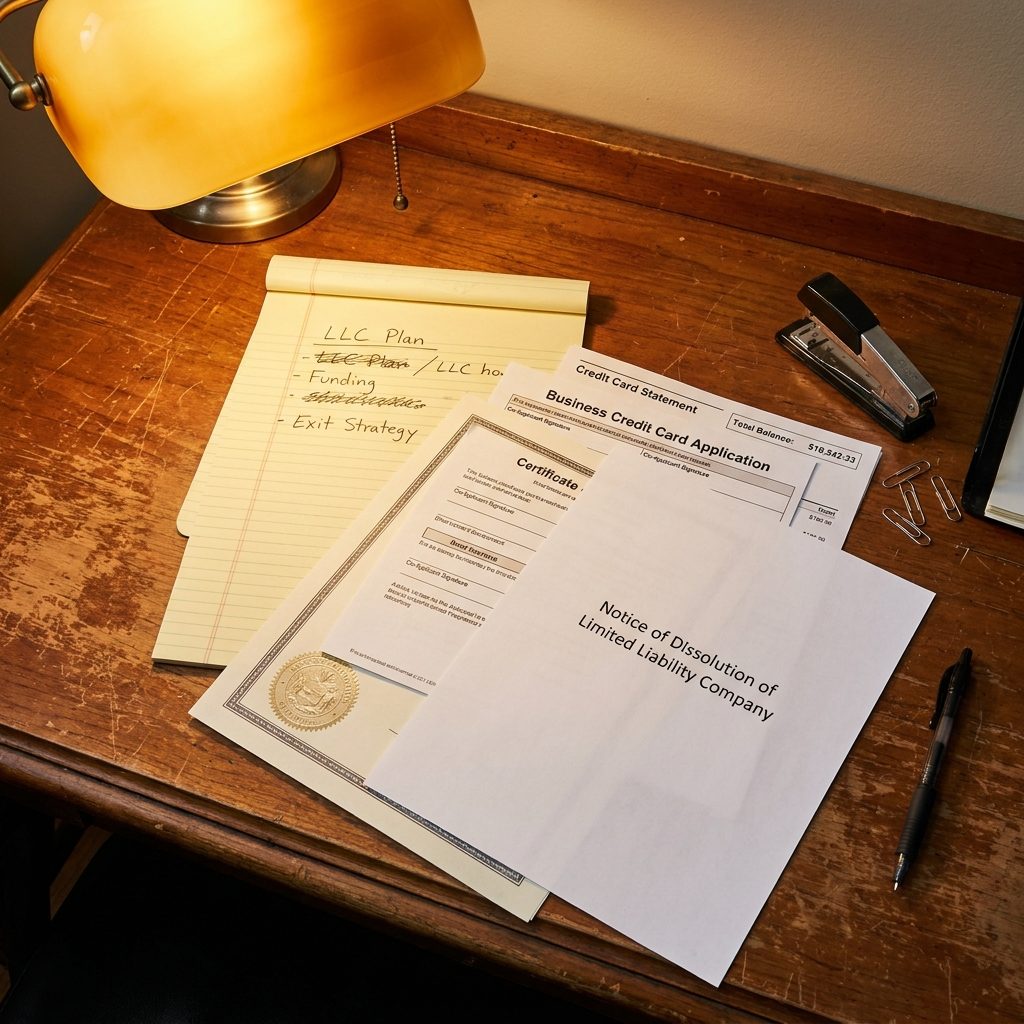

Business Debts from an LLC That Was Dissolved Without Warning

The business sounded like partnership. In practice, the survivor’s name and Social Security number provided the credit access and the liability, while the abuser ran every operational decision. When the relationship ended, the LLC got dissolved, sometimes without telling the survivor, sometimes through a filing the survivor unknowingly signed.

Business debts don’t always appear on personal credit reports immediately. They arrive later, through business credit reporting agencies or personal guarantees buried in vendor contracts. Survivors who had no idea they were listed as a business owner find out when a supplier or landlord sends a collections notice to their home address.

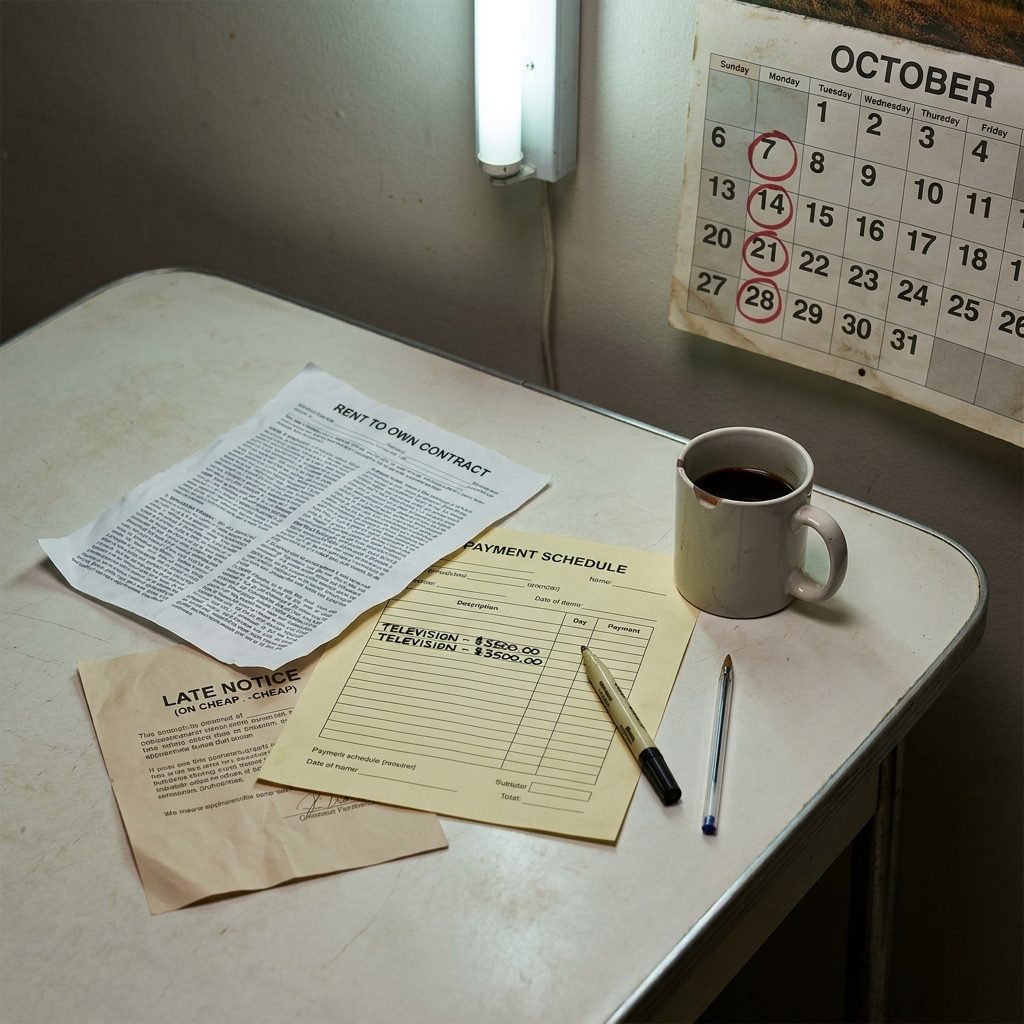

The Rent-to-Own Trap Nobody Told You About

Would you like to save this?

Rent-to-own stores don’t require a credit check, which is exactly why abusers use them. A television, a washer, a laptop, signed in the victim’s name while the abuser kept the item. Months later, the collections calls start. The account never appeared on a credit card statement because it wasn’t a card. It was a contract. And contracts for rent-to-own debt often don’t show up until they go to collections and land on a credit report like a small explosion.

A Store Credit Card Opened at the Checkout Register

A ten-percent discount. That’s what it costs. An abuser at a register, victim’s ID in hand, opens a store card in under three minutes while the cashier pitches the savings. The card leaves the store with the abuser. Charges accumulate across months. The victim never sees a statement because the billing address was changed at sign-up.

Store cards from major retailers are among the most common hidden accounts survivors find, precisely because they’re so easy to open, no hard approval process, no waiting period, no paperwork sent home.

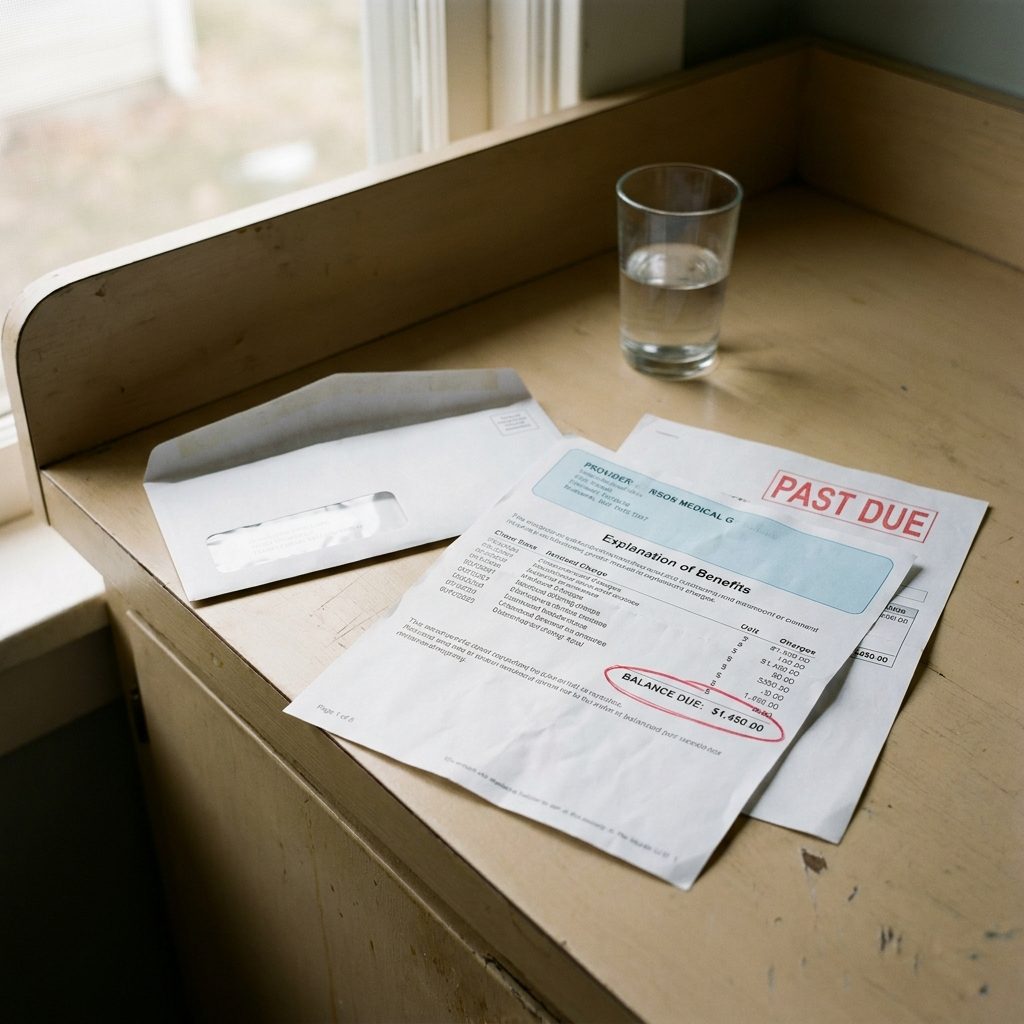

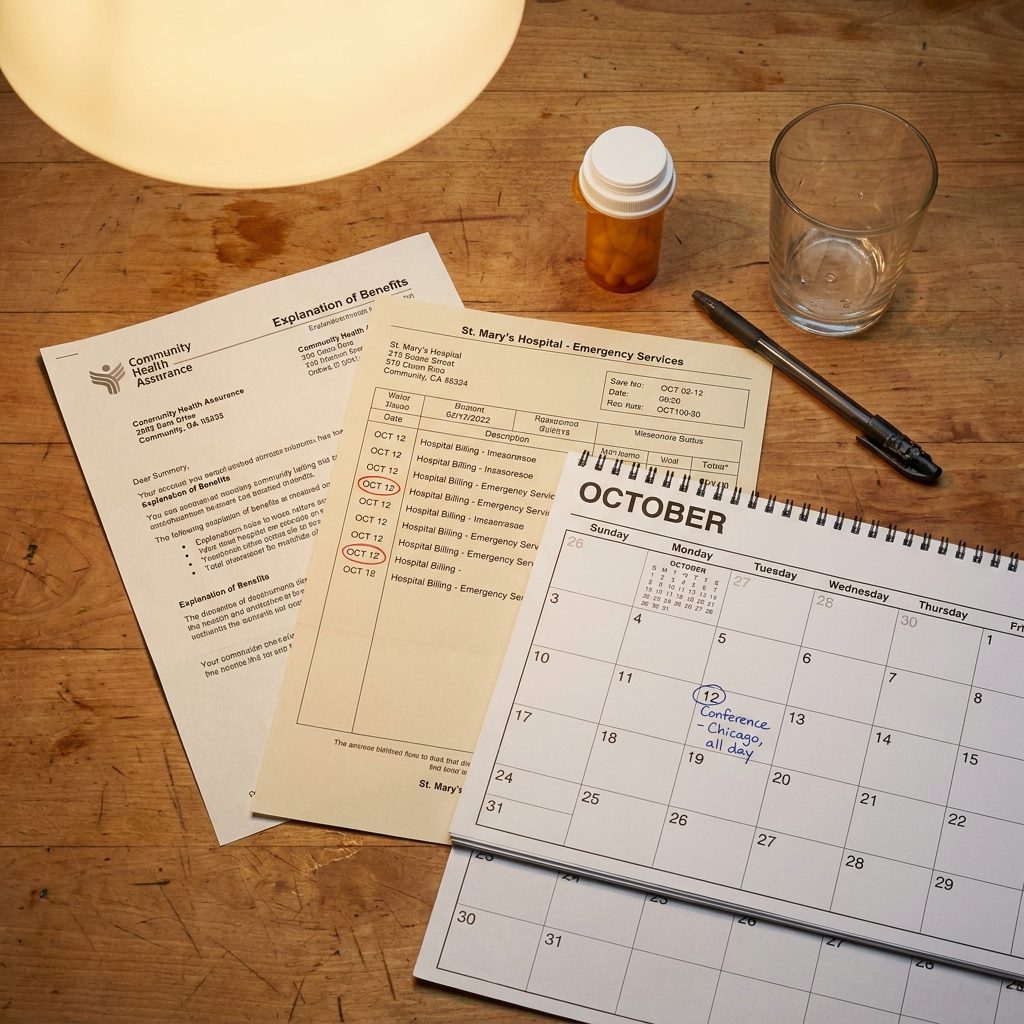

Medical Debt From Appointments the Victim Never Attended

Medical debt shows up in names of people who never missed a doctor’s appointment in their life, because someone else used their insurance and their identity to get care. A visit to an urgent care clinic, a prescription pickup, a specialist appointment. Billed to the victim’s insurance, balance sent to their address (which the abuser controlled), ignored until it hit collections.

Healthcare billing is slow. These debts can take eighteen months to surface. By then, the relationship is over, the abuser is gone, and the survivor is left explaining to a collections agent why they owe for a procedure they never received.

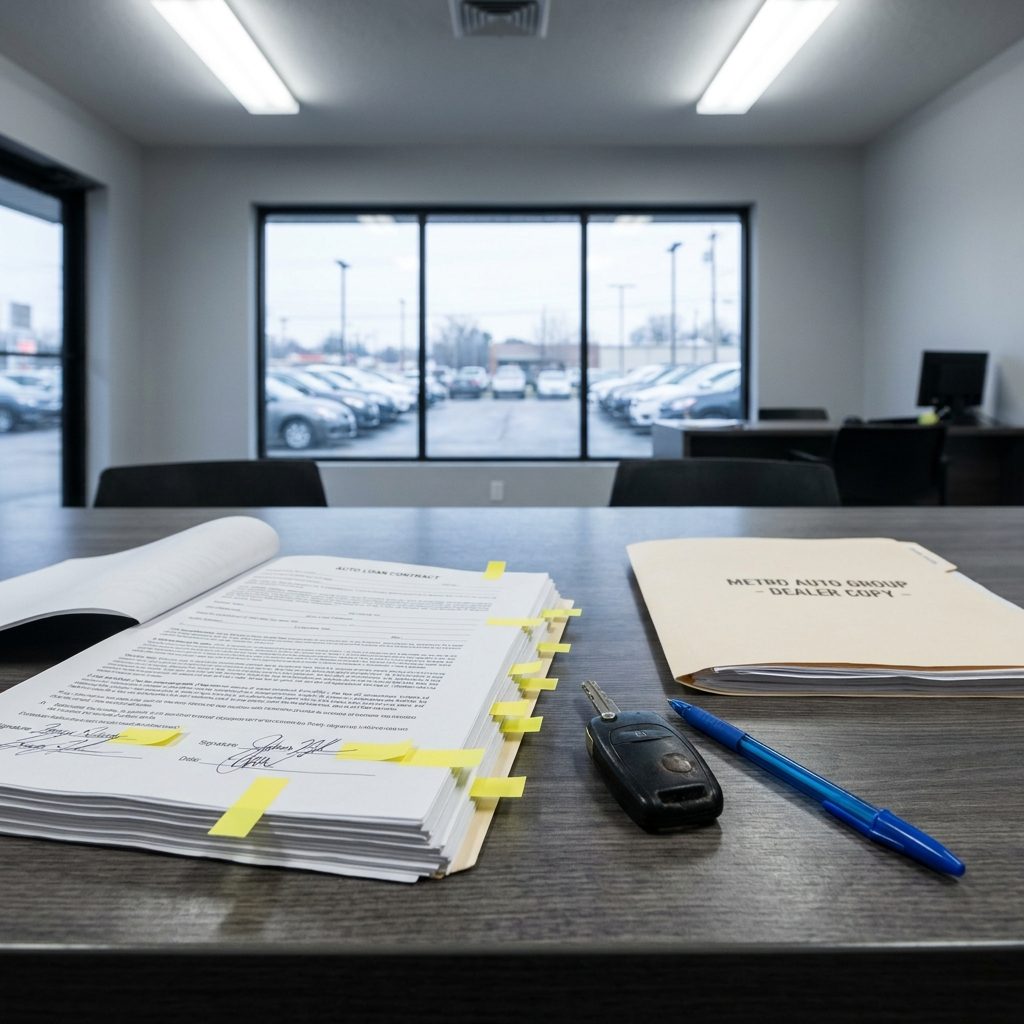

The Car Loan Where the Abuser Drove and the Victim Signed

The victim signs because they have the better credit score. The abuser drives. This arrangement is presented as practical, maybe even generous, the abuser gets to work, the family has a car. Eighteen months later, when the relationship ends, the survivor discovers the car left with the abuser and the payments stopped. The loan is in their name alone. The repossession, the deficiency balance, all of it lands on one credit report.

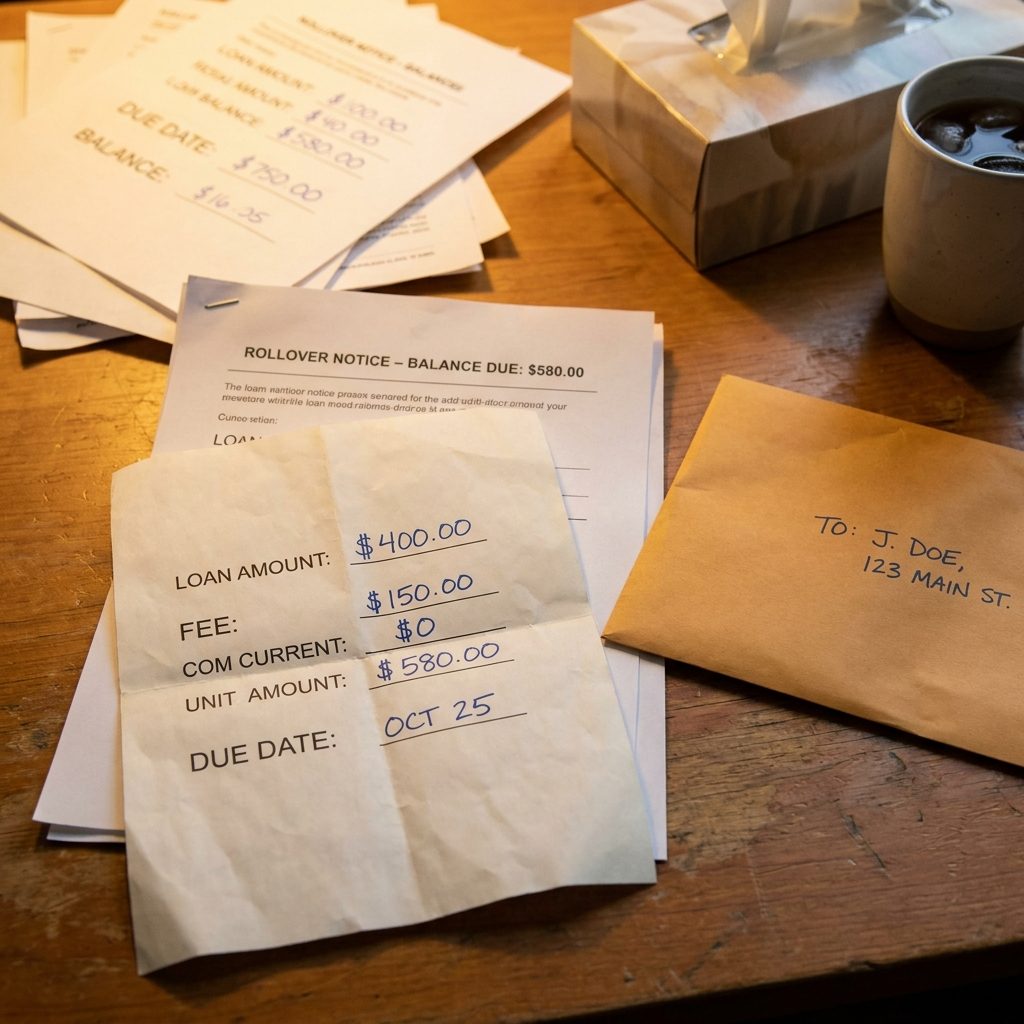

A Payday Loan Rolled Over So Many Times Nobody Remembered the Original Amount

Payday loans are designed to roll over. That’s the business model. An abuser takes out a small loan in the victim’s name, pays the rollover fee but never the principal, and the debt compounds across months. The original three hundred dollars becomes eight hundred. The thermal-paper contracts pile up at an address the victim never controlled.

These loans often don’t appear on credit reports immediately, some payday lenders don’t report to the bureaus until default. Which means the survivor has no warning until the collections account appears, fully formed, months after the relationship ended.

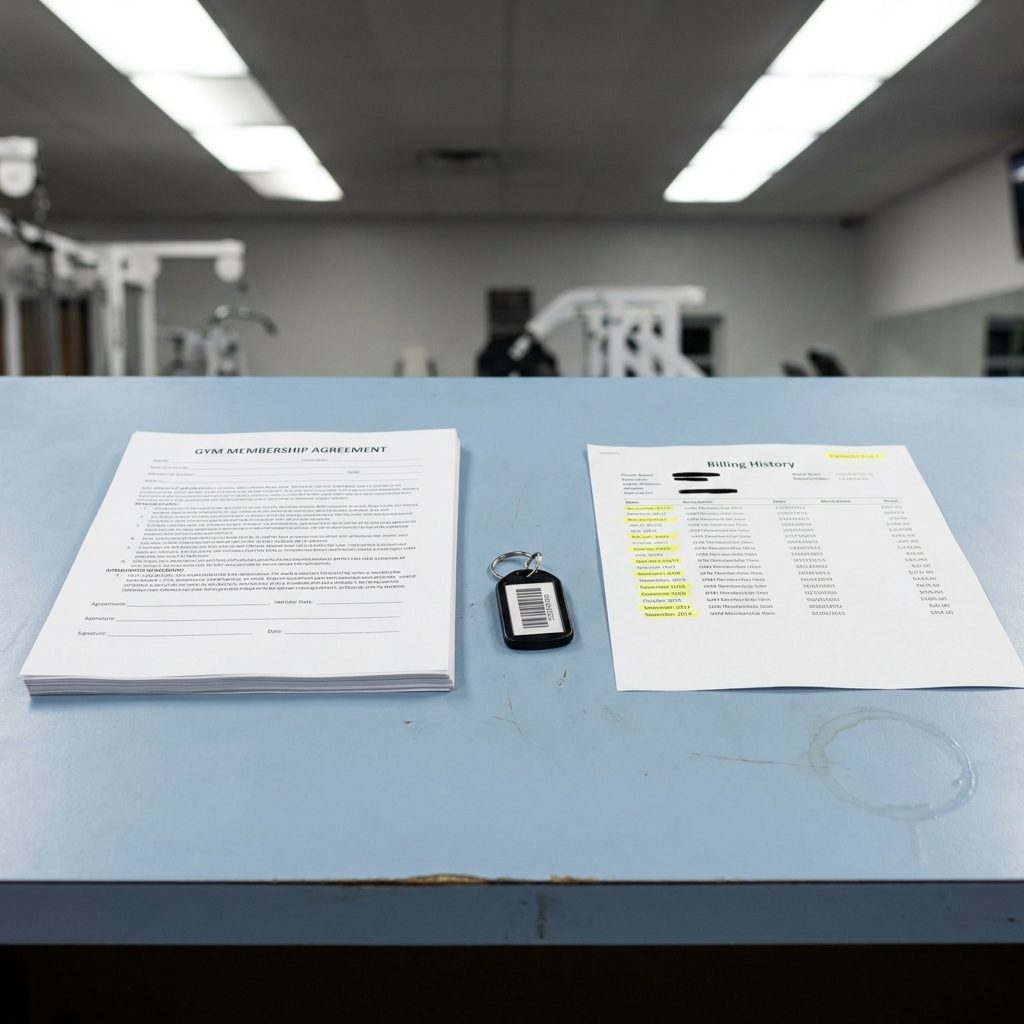

A Gym Membership That Billed Quietly for Two Years

Gym memberships are notoriously hard to cancel, and abusers know it. A membership opened in the victim’s name auto-bills monthly, quietly, for years. The abuser uses the facility. The charge is small enough, thirty, forty dollars a month, that it gets lost in a bank statement. Survivors often find these accounts only when they pull a full transaction history and notice a recurring charge to a gym in a city they haven’t lived in for two years.

The Utility Account That Stayed On After the Move

When the survivor left, the utilities stayed in their name at the old address. The abuser kept living there. The electric bill, the gas, the water, all billing to an account the survivor opened years ago and never closed because they didn’t know they could, or because the abuser controlled the process of leaving.

Utility debt in collections is one of the first things a landlord checks. Survivors trying to rent a new apartment find the application flagged for hundreds or thousands of dollars in unpaid utilities at an address they fled. The system treats it as a choice, not a trap.

A Business Credit Card Opened on an LLC the Victim Co-Signed and Forgot

The abuser had a business idea. Or said they did. The survivor co-signed on the LLC paperwork because they were told it was for both of them, a shared future. A business credit card followed, in both names. The business never really operated. The card did.

When the relationship ended, the LLC dissolved on paper, but the debt didn’t. Business credit card debt tied to a closed LLC can still chase individual co-signers for years. Survivors who didn’t know they’d co-signed anything find out the hard way that their signature on a business document is just as binding as one on a personal loan.

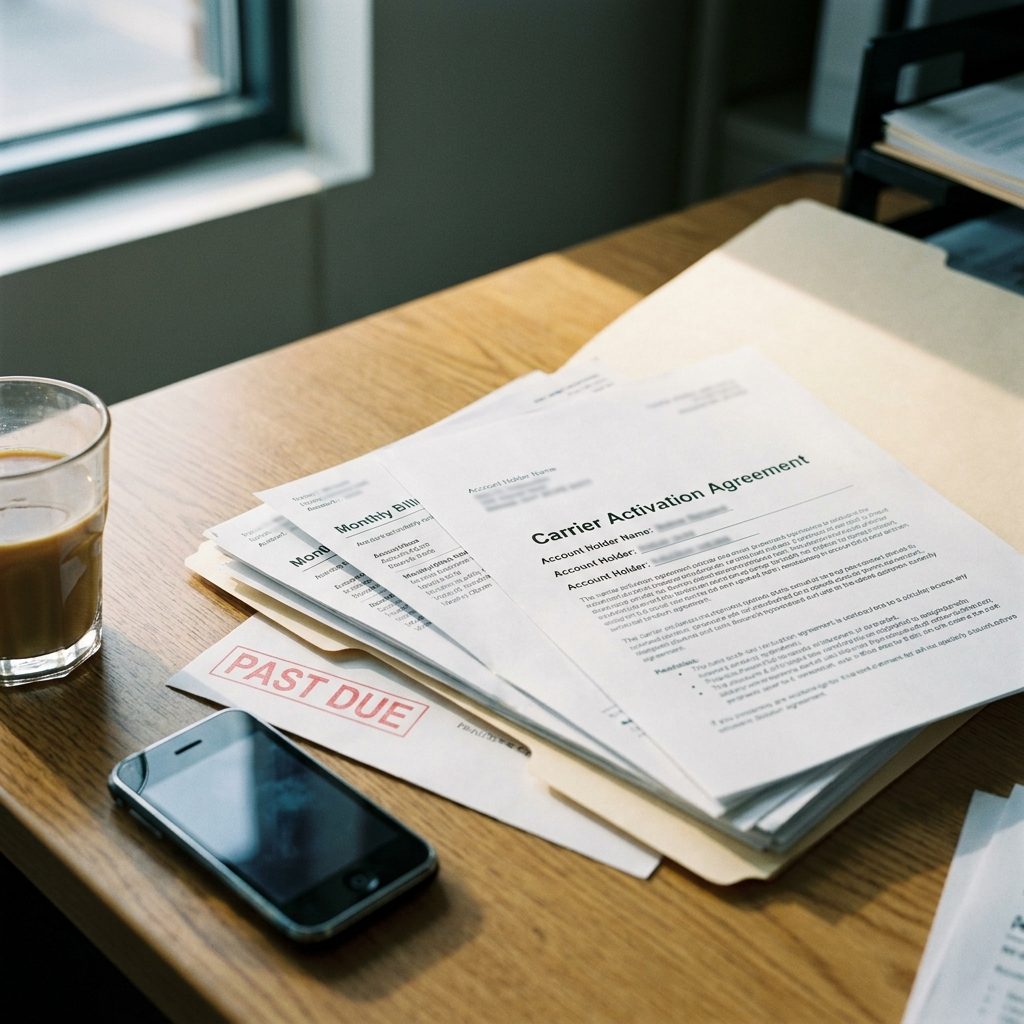

The Cell Phone Plan Opened in Your Name You Never Once Used

Wireless carriers let one account holder add lines, and abusers use that window freely. The line gets opened in the survivor’s name, handed to a family member, a girlfriend, sometimes no one at all, and the bill goes unpaid for eighteen months before collections shows up on a credit report. By then the original carrier account has been closed, the number disconnected, and there’s no record of who actually used the phone. Just the debt, in one name.

A Second Mortgage Nobody Mentioned Until the House Was Already Gone

Home equity lines of credit require both signatures on a jointly owned property, but forged signatures happen, and notarization fraud is more common in financial abuse cases than most people realize. Survivors sometimes learn about a second mortgage only after receiving a foreclosure notice, or when a title search surfaces the lien during a sale they initiated. The original loan proceeds were spent long before the paperwork surfaces.

The Rent-to-Own Contract Signed for Furniture in a Place You Never Lived

Would you like to save this?

Rent-to-own stores run informal credit checks, but they issue contracts easily, and the contract holder is the one chased when payments stop. A sofa, a laptop, a washer-dryer set: these show up on specialized consumer reporting databases like the Rental Exchange, and unpaid rent-to-own balances get sent to collections agencies that report to all three bureaus. The survivor never sat on the furniture. They just signed for it once.

Medical Bills From an Emergency Room Visit That Happened While You Were Somewhere Else

Medical identity theft inside intimate relationships often goes undetected for years because survivors don’t request annual benefits summaries and insurers don’t flag the misuse proactively. An abuser uses a partner’s insurance card, a dependent’s social security number, or both. The bills that get sent to collections are for services the survivor never received. Disputing them requires a full fraud report, a formal investigation by the insurer, and often a police report, a process that can take six months or longer.

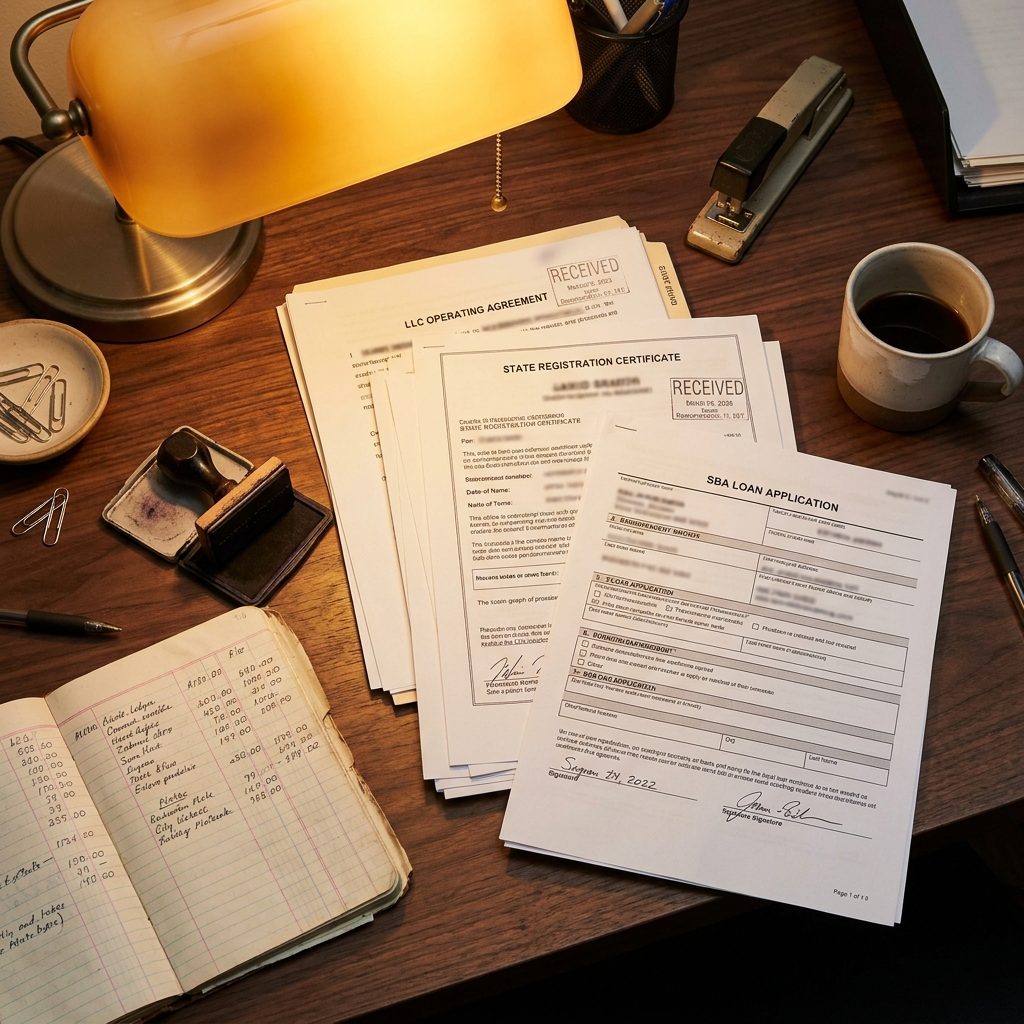

The Small Business Loan Taken Out on an LLC You Didn’t Know Existed

Forming an LLC in most states requires only one person’s name and a filing fee. In community property states, a spouse’s financial history can be tied to business debts even if they never signed the loan documents. Survivors sometimes discover they were listed as a co-owner or registered agent on a business entity they knew nothing about, which means the SBA loan, the equipment financing, or the merchant cash advance taken out under that business becomes their problem when the lender comes looking.

Gym Memberships and Subscription Boxes That Kept Billing for Years on Autopay

These aren’t the dramatic debts. They’re the quiet ones. A gym membership with a 12-month minimum. A streaming bundle. A monthly beauty box ordered once and never cancelled. Charged to a card in the survivor’s name, billed to an address they haven’t lived at in two years, auto-renewed every month. Individually small, collectively they can total hundreds of dollars, and if the card goes over limit from accumulated charges, the late fees and interest stack fast.

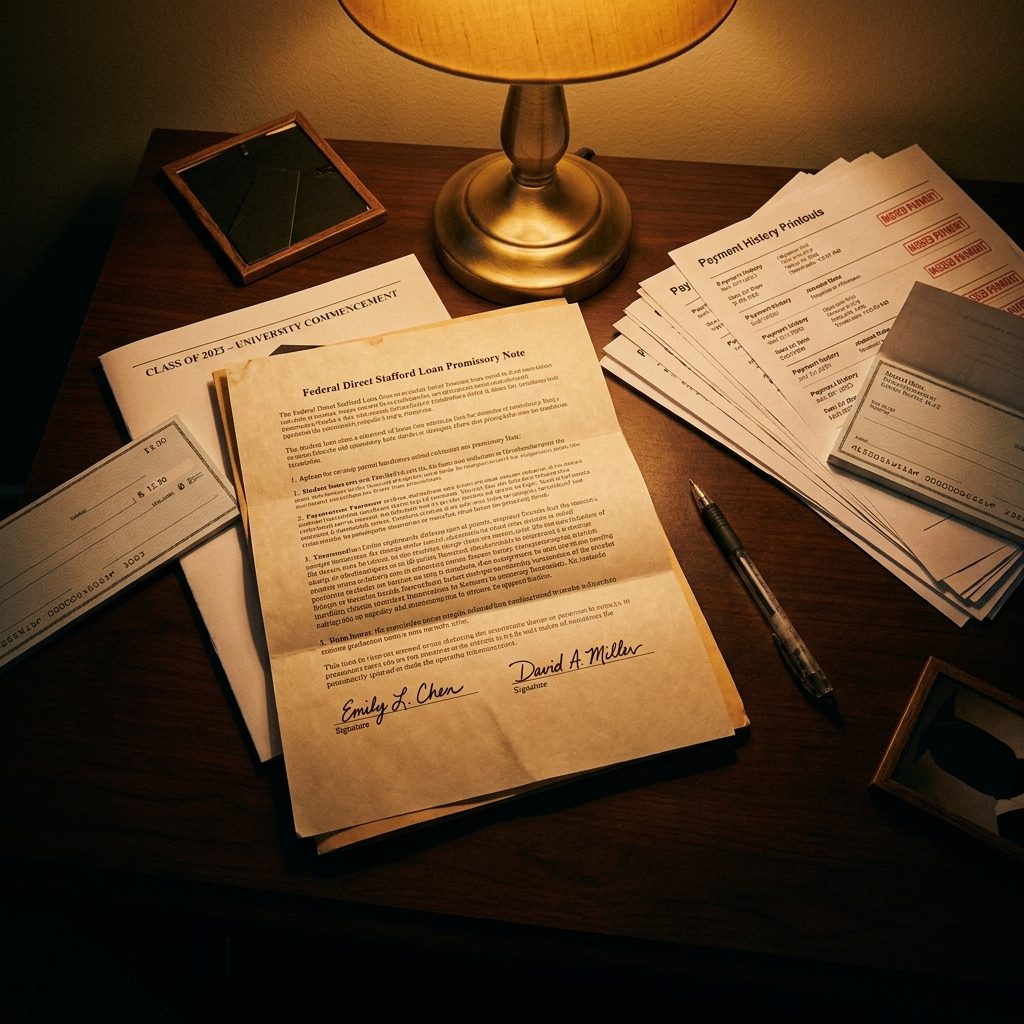

The Co-Signed Student Loan Whose Payments Stopped the Month After Graduation

Co-signing a student loan feels like support. It becomes a liability the moment the primary borrower stops paying and the servicer starts reporting both names to the credit bureaus. Co-signers are equally responsible for the full balance, not just their half, the whole thing. Release programs exist, but they require the borrower’s cooperation, a clean payment record, and sometimes years of qualifying payments first. None of those conditions are easy to meet when the relationship has ended badly.

A Car Loan From a Buy-Here-Pay-Here Lot Still Running Four States Away

Buy-here-pay-here dealerships don’t always report to major credit bureaus when payments are current, but they almost always report when accounts go delinquent, and they sell defaulted contracts to third-party collectors who do. A survivor co-signs for a vehicle as a favor, the car ends up in another state, payments stop, and six months later a collections account appears for $6,400. The car may have been repossessed and resold. The deficiency balance stays.

The Auto Policy on a Car You’ve Never Seen

Auto insurance premiums get quietly charged to a credit card or bank account, and the policy lists an address you’ve never lived at. The car itself, sometimes a vehicle you can’t identify by VIN, may have been used as collateral elsewhere. Survivors frequently discover they were listed as the primary insured on vehicles their abuser titled, insured, and drove without their knowledge. The monthly charge looked small enough to miss. The liability exposure is not small at all.

A Store Credit Card Opened the Day You Were in the Hospital

The account open date is the detail that breaks people. It’s a Tuesday in March, or a Monday in October, and when they look at their calendar from that year, they realize they were in a hospital bed, or a shelter, or somewhere so far from a retail checkout line that the timing is impossible to explain as coincidence.

Store cards are easy to open with a name, a Social Security number, and a date of birth. The credit limits are often low enough that the accounts stay off the radar for months, sometimes until a collections notice arrives at a parent’s address.

The Payday Loan That Rolled Over Sixteen Times Without You Knowing

Payday lenders are required to report to credit bureaus, but the reporting often lags by months. By the time the account surfaces on a credit pull, it has rolled over so many times that the original loan amount is unrecognizable buried under fees. Survivors find these accounts in collections, often from lenders operating under names they don’t recognize because the original lender sold the debt twice before it landed.

The abuser’s logic was simple. A $300 loan costs very little to open in someone else’s name. The rollover fees, sometimes exceeding the original principal within two months, become someone else’s problem entirely.